Russian oil exports in March: increasing in value despite damaged Baltic sea ports

Russian oil exports in March 2026 were marked by disruptions in the Baltic Sea region, mainly due to a wave of Ukrainian drone attacks that hit the strategic ports of Primorsk and Ust-Luga hard. Although Russia compensated for lost volumes financially thanks to high world market prices.

Despite the disruptions, total revenues from fossil fuel exports in March rose by 52% compared to February, mainly driven by sharply rising global oil prices due to conflicts in the Middle East. However, overall export volumes increased more modestly by around 16% .

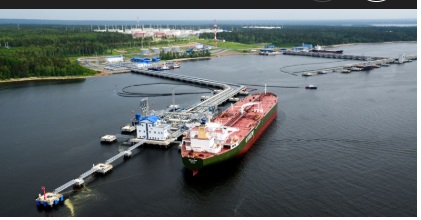

Primorsk and Ust-Luga

During the last week of March (from around March 23), oil loading at Russian Baltic Sea ports decreased by a whopping 53% compared to the same period last year.

Primorsk: The port, which normally handles nearly 1% of global oil supply, was hit by attacks that damaged about 40% of its storage capacity . Satellite images showed extensive damage to oil reservoirs, forcing a shutdown.

Ust-Luga: The port was hit even harder. Export volumes fell by 74% in the last nine days of March compared to the previous year. An attack on March 25 knocked out key rail unloading infrastructure, halting the flow of oil products from several Russian refineries (including Kirishi).

March 26–27 marked the first time since the beginning of the invasion in 2022 that no Russian oil ships were loaded at the major Baltic Sea ports for two consecutive days.

Logistics are tight

Ice restrictions: Lack of ice-classified vessels limited the availability of tankers in the Baltic Sea.

Shadow Fleet: Approximately 48% of Russian seaborne oil was transported in March by the so-called “shadow fleet” to circumvent sanctions.

Refinery shutdown: Damage to the Kirishi refinery led to a complete halt in production of fuels for export at the end of the month.

The second week of April 2026 (around April 6–13) saw Russian oil exports from the Baltic Sea experience an unstable recovery following the massive disruptions at the end of March. Despite attempts to resume normal operations, logistical problems and new attacks continued to hamper volumes.

Primorsk: Partial recovery

Primorsk, which suffered an attack on a supply pipeline on April 5 , showed signs of a fragile return to operation in the second week of the month.

Volume trend: After exports essentially came to a standstill in early April, individual tankers began to be loaded again around April 6–7.

Price development: Paradoxically, the price of Urals oil in Primorsk reached a 13-year high of over $116 per barrel in early April. This was due to a global supply shock rather than Russian strength.

Status: The port was operating but with reduced capacity due to damage to warehouse and pipeline infrastructure.

Ust-Luga had a significantly more difficult second week of April than Primorsk.

New attacks: Just as the port was attempting to resume operations on April 6 (after being down since late March), new drone attacks were reported on the night of April 7. This forced new temporary shutdowns.

Loading statistics: During the week ending April 5, the number of tanker departures from the Baltic Sea (Primorsk and Ust-Luga combined) fell from an average of 11 to just 7 per week . The trend remained downward or flat during the following week.

Logistical bottleneck: Exports of oil products (diesel and naphtha) from Ust-Luga were virtually paralyzed. Refineries that normally ship via the port were forced to seek more expensive rail routes to ports such as Vysotsk or Taman on the Black Sea.

Declining/Low. Still about 30–40% below normal levels.

Operational status

Intermittent. Outages due to flight alarms and repairs are ongoing in parallel.

Destinations

India (59%) dominates the few cargoes that do leave, followed by Turkey (16%).

Income

High per barrel, but low in volume. The high oil prices partly masked the physical export crisis.

Day by day

By mid-April 2026, the Russian strategy was to prioritize the “shadow fleet” (tankers without Western insurance) to be able to quickly load and leave ports between attack waves, despite the increased risks of environmental accidents in the Baltic Sea.

March 2026: The Great Shutdown

March marked the beginning of a ”black month” for Russian logistics, where drone attacks knocked out large parts of capacity.

March 23: First major wave of attacks hits Primorsk . Satellite images show fires at Transneft’s tank farm. Exports slow dramatically.

March 25: Ust-Luga is attacked. Damage is reported to the rail terminal and Novatek’s condensate plant. All loading is completely stopped.

March 26–27: For the first time since 2022, both ports are completely at a standstill for two days. Primorsk is attacked again on the 27th.

March 31: Another attack on Ust-Luga (the fifth in ten days). By the end of the month, export volumes from Ust-Luga had fallen by 74% compared to the previous year.

Primorsk

April 2026: Fragile recovery

During April, Russian authorities attempted to repair the damage, but were met with continued attacks.

April 1–4: Attempts to resume minimal operations. Bloomberg reports that individual tankers begin loading under strict blackout and electronic jamming.

April 5: Primorsk is hit again. Three large storage tanks (20,000 m³ each) are damaged in a major fire.

April 7: Ust-Luga is subjected to a nighttime attack. At least three storage tanks at Transneft-Baltika catch fire. This occurs just as the port has begun to return to “minimum levels.”

April 10–13 (Second week):

Trend: An uncertain recovery is beginning. The number of tanker departures in the Baltic Sea remains around 30–40% below normal levels .

Logistics: Russia is forced to redirect oil via rail to smaller ports and the Black Sea, which increases costs significantly.

Economy: Despite the volume loss, revenues per barrel are reaching record levels (over 115 USD ) due to global concerns, which partially hides the physical crisis in the statistics.

Status mid-April

Port

Status

Damage level

Primorsk

Limited operation

Approximately 30–40% of storage capacity is out.

Ust-Uga

Very unstable

Frequent stops; major damage to railways and product terminals.

Export volume

Low

Weekly deliveries down by about 50% compared to April 2025.